While Nifty took 21 years to increase from 1000 to 10000, here's someone telling us that it will increase to 100000 sooner than that. Well, it might as well be. At the same time, we cannot stop people from saying something, right? When there is demand, supply comes naturally. There is a lot of euphoria these days; so anything that attracts headline is game.

Of course, both political and economic environments are far better as of now. So returns from the Indian equities are going to be much better than any other alternative investment opportunities. Nevertheless, we need to be aware of the pricing game and the value game; both are different.

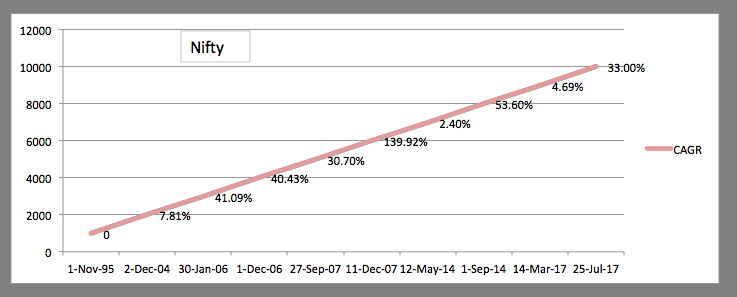

How about making an annualized return of 139.92%? Nifty increased from 5000 in September 2007 to 6000 in December 2007. This happened even while the index was 22.49 times earnings and 5.33 times book equity. Extrapolating, or hoping for the repetition of historical returns, there is an expectation of similar returns now. That's because Nifty is trading at more than 25 times earnings, and more than 3.5 times book equity.

Well, the story is not complete. What happened after December 2007 is important. Another 1000 points increase to 7000 happened only in May 2014. The annual return over more than 6 years was 2.40%. Yeah, there was the great financial crisis in the middle. But then at 6000, the index was quoting at more than 26 times earnings, and more than 6 times book equity. If you know that your returns are hugely dependent upon the price you pay, you would realize what it means to buy in December 2007.

Of course the buyer in May 2014 at 7000 was hugely rewarded leading the index up to 8000. But not the one at September 2014, who thought 8000 was a bargain at less than 21 times earnings and less than 3.5 times book, for the annualized return was only 4.69%; even after holding it until 10000, the annualized return is only 7.89%.

During boom times, as it is now, there will be a number of idiots talking about, what else, boom. The exuberance tends to be irrational. As someone said, it is only when the tides are gone you will know who is left naked. I reckon, these days there are more men and women naked than those who are not. We will only find that out much later after the bulls are tamed, and bears march in.

It is also good to know that change from 1000 points to 2000 is a 100% increase; and from 9000 to 10000 is an increase of just over 11%. Yet, people talk as if both increases are similar. The optimism in the tone is apparent. The index took only 4 months to increase from 9000 to 10000 in July 2017; that's an annualized return of 33%.

Unfortunately, people don't see the fundamentals underlying the index value. You cannot make more than what the business behind the stock makes in the long run; and equity investing is for the long run, for businesses are meant to be run for long. If the business is making say, 15% on capital in the long run, any expectation of more than that from the stock market is unrealistic. Stock prices follow business eventually. Of course, anything can happen in the short run. Yet we have people putting their hard-earned money into things that they don't understand. They will take time to check smart phone prices, but not stock prices. Heck...

Some perspective: To bring the earnings multiple down to say, 20, the Nifty earnings will have to increase by 25%, and its value will have to remain at 10000. Will that happen in the near future? I don't know about that; but, what I know is that the earnings will have to go up more than the index itself in the coming years in order to give a reasonable return to the buyers at the current level.

It's time to get real, I guess.