The company makes tapered roller bearings (71%) and AP cartridge tapered roller bearings (21%), and it also trades in other types of bearings. The traded bearings are sourced from its group companies globally. The company also provides maintenance and refurbishment services.

Its growth largely depends upon that of manufacturing and infrastructure sectors. It has manufacturing facilities in Jamshedpur and Raipur which mainly cater to medium and heavy trucks, off-highway equipment, railways and exports.

Its growth largely depends upon that of manufacturing and infrastructure sectors. It has manufacturing facilities in Jamshedpur and Raipur which mainly cater to medium and heavy trucks, off-highway equipment, railways and exports.

As per management, the current size of anti-friction bearings market is approximately Rs.95 b, of which automotive industry has 45% share and industrial sector has 55%. The company had revenues of Rs.10.62 b for the year ended March 2016. So there is space to grow.

The management also notes that low quality and counterfeit in the market and volatility in prices of metal components (main raw materials: steel, rings and accessories) as major threats to its business. Yet, it appears to be excited about the government's planned expenditure in building road and rail infrastructure corridor, private participation in defense and allied sector, and electrification drive.

Timken India is currently valued by the market at Rs.38.57 b. Timken Singapore Pte holds 75% of shares in the company; the ultimate holding company is The Timken Company, USA, which is worth $2.69 b as priced by the market.

Timken India pays royalty to its holding company; for 2016 it paid Rs.222 m, which is approximately 2% of revenues. It also pays inter-company service charges to the group companies.

It has 68 m shares outstanding. Apart from the institutional placement of 4.26 m shares at Rs.120 per share in 2014, the company has never diluted its shares. The placement had to be done to bring down the shareholding of the parent to 75% to adhere to the regulatory guidelines.

The company never dividends until 2012 when it made a hefty payout of Rs.1.27 b. Then in 2014 it paid dividends of Rs.6.50 per share (remember dilution of the holding company's equity); for 2016, it paid Rs.1 per share. Timken does not have a reliable payout policy yet.

Timken India pays royalty to its holding company; for 2016 it paid Rs.222 m, which is approximately 2% of revenues. It also pays inter-company service charges to the group companies.

It has 68 m shares outstanding. Apart from the institutional placement of 4.26 m shares at Rs.120 per share in 2014, the company has never diluted its shares. The placement had to be done to bring down the shareholding of the parent to 75% to adhere to the regulatory guidelines.

The company never dividends until 2012 when it made a hefty payout of Rs.1.27 b. Then in 2014 it paid dividends of Rs.6.50 per share (remember dilution of the holding company's equity); for 2016, it paid Rs.1 per share. Timken does not have a reliable payout policy yet.

What is interesting is that the market has steadily increased its expectations about the company and accordingly, its price over the last decade.

At the current price of Rs.569.65, the stock is trading at over 42 times its earnings. Although the PE multiple is a pricing measure, it can also be analyzed based upon the intrinsic value of a business. What we get out of the exercise is the implied PE multiple. For instance, if the value of the business is 100 and its earnings are 5, the implied multiple is 20.

So then there had to be some fundamental change in the business affairs of Timken India for the multiple to expand.

Revenues grew at a cagr of 18.06% in the last 5 years and 12.37% in 10 years. We can choose to ignore the minor variation caused by the change of its financial year end from December to March from 2012 onwards.

Operating income grew at 20.64% and 10.43% during the respective periods; and earnings for common grew at 12.48% and 9.20%.

EPS grew at a slightly lower rate due to the institutional placement in 2014; it grew at 11.03% annually in the last 5 years and at 8.49% in the last 10 years.

That's the past. What we are really interested in is the future story for the business. How much can the revenues grow in the next 5 years? For the moment, let's expect to grow at 20% per annum. During the stable growth period the business cannot grow at a rate higher than the long term growth rate of the economy; therefore, let's set the perpetual growth rate to reflect that.

Operating margins started declining since 2006, but have increased in the last 2 years. Let's expect Timken to better its margins in the future and reach to 15% as a stable business. Note that this margin is expected to be perpetual and therefore sustainable.

2012 had a triple advantage: 15-month period; higher revenues and operating income; and lower operating capital. Therefore the return on capital was much higher. From 2012 onwards, the company spent approximately Rs.3 b in reinvestment; higher capex for expansion projects and also higher working capital requirement. In the previous 6 years, the aggregate reinvestment was Rs.602 m. Let's hope that Timken will be able to maintain a return on capital of 25% as a stable business.

Revenue growth rate of 20% is not going to come easy and free. There has to be right amount of reinvestment. Timken has already planned capacity expansions for railway bearings at Rs.1.24 b, and for tapered roller bearings at Rs.643 m, both at Jamshedpur plant. At 2.33 times capital turnover, the reinvestment is going to be there each year. Let's expect Timken to reach the stable growth period after 10 years of high growth.

Timken has generated free cash flows to firm of Rs.1.55 b in the last decade.

Where does it all end? Based upon our expectations, the projected numbers show that the invested capital is set to grow at 15.21% in the next decade compared to the historical rate of 12.73%; operating income at 16.70% compared to 10.43%; and FCFF at 37.96% compared to 29.96%.

Timken had excess cash of Rs.334 m as of March 2016 and investments in mutual funds of Rs.384 m, the market value of which should be higher. It had debt of Rs.63 m including interest-bearing deposits from dealers and distributors. It also had contingent liabilities (sales tax, income tax, excise, customs and other claims) of Rs.219 m; how much of this is going to be cash outflows is left for us to estimate.

Now the value of Timken's operating business becomes a function of our expected rate of return. If we accept that our expectations of 20% revenue growth, 15% operating margin and 25% return on capital are sustainable, the stock is currently priced (at Rs.569.65) by the market to give a return of 9.23% in the long term. Is that rate of return reasonable?

I would rather ask, is 15% operating margin sustainable for the business? Timken has never reached that in the last 10 years. I would also ask, can it increase its revenues by 4 times its current revenues by 2026? Will the market be able to accommodate that? Then there is the philosophical question, what happens if our expectations about the business and market turn out to be all wrong?

How about some sensitivity? If we tweak a little bit and change revenue growth rate to 15% and sustainable operating margin to 12%, the expected return falls to 7.65%.

If we consider that intrinsic valuation through discounted cash flows is too complex involving estimates of cash flows and growth rates, which we are incapable of being correct, we need not tread that path. We can bring the number of years far less than perpetual and try to price the stock.

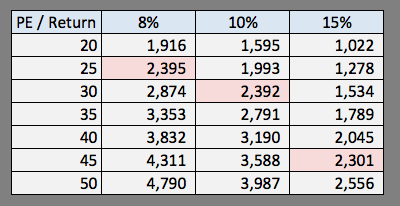

Timken earned Rs.13.52 per share in 2016. The price of the stock becomes a function of growth rate in earnings, the multiple at which we expect it to trade and our expected rate of return. Conversely, we can keep the current price of the stock constant (the less we argue with the market, the better) and calculate the expected rate of return.

If we expect earnings per share to grow at 12% in the next 10 years and the stock to trade at 40 times, the stock at its current price would give an annual return of 11.42%. If growth rate is 15%, the rate of return is going to be 14.40%. That's a profound story, isn't it?

So what if earnings grow at 10% and the stock trades at a multiple of 25? Do we like to earn 4.40% in the next decade? At 11% growth rate, which is the last 5-year average, with a multiple of 40, the rate of return is going to be 10.42%; at 8.50%, which is the last 10-year average, the rate of return is 7.93%. Such is life.

That's the past. What we are really interested in is the future story for the business. How much can the revenues grow in the next 5 years? For the moment, let's expect to grow at 20% per annum. During the stable growth period the business cannot grow at a rate higher than the long term growth rate of the economy; therefore, let's set the perpetual growth rate to reflect that.

Operating margins started declining since 2006, but have increased in the last 2 years. Let's expect Timken to better its margins in the future and reach to 15% as a stable business. Note that this margin is expected to be perpetual and therefore sustainable.

2012 had a triple advantage: 15-month period; higher revenues and operating income; and lower operating capital. Therefore the return on capital was much higher. From 2012 onwards, the company spent approximately Rs.3 b in reinvestment; higher capex for expansion projects and also higher working capital requirement. In the previous 6 years, the aggregate reinvestment was Rs.602 m. Let's hope that Timken will be able to maintain a return on capital of 25% as a stable business.

Revenue growth rate of 20% is not going to come easy and free. There has to be right amount of reinvestment. Timken has already planned capacity expansions for railway bearings at Rs.1.24 b, and for tapered roller bearings at Rs.643 m, both at Jamshedpur plant. At 2.33 times capital turnover, the reinvestment is going to be there each year. Let's expect Timken to reach the stable growth period after 10 years of high growth.

Timken has generated free cash flows to firm of Rs.1.55 b in the last decade.

Where does it all end? Based upon our expectations, the projected numbers show that the invested capital is set to grow at 15.21% in the next decade compared to the historical rate of 12.73%; operating income at 16.70% compared to 10.43%; and FCFF at 37.96% compared to 29.96%.

Timken had excess cash of Rs.334 m as of March 2016 and investments in mutual funds of Rs.384 m, the market value of which should be higher. It had debt of Rs.63 m including interest-bearing deposits from dealers and distributors. It also had contingent liabilities (sales tax, income tax, excise, customs and other claims) of Rs.219 m; how much of this is going to be cash outflows is left for us to estimate.

Now the value of Timken's operating business becomes a function of our expected rate of return. If we accept that our expectations of 20% revenue growth, 15% operating margin and 25% return on capital are sustainable, the stock is currently priced (at Rs.569.65) by the market to give a return of 9.23% in the long term. Is that rate of return reasonable?

I would rather ask, is 15% operating margin sustainable for the business? Timken has never reached that in the last 10 years. I would also ask, can it increase its revenues by 4 times its current revenues by 2026? Will the market be able to accommodate that? Then there is the philosophical question, what happens if our expectations about the business and market turn out to be all wrong?

How about some sensitivity? If we tweak a little bit and change revenue growth rate to 15% and sustainable operating margin to 12%, the expected return falls to 7.65%.

If we consider that intrinsic valuation through discounted cash flows is too complex involving estimates of cash flows and growth rates, which we are incapable of being correct, we need not tread that path. We can bring the number of years far less than perpetual and try to price the stock.

Timken earned Rs.13.52 per share in 2016. The price of the stock becomes a function of growth rate in earnings, the multiple at which we expect it to trade and our expected rate of return. Conversely, we can keep the current price of the stock constant (the less we argue with the market, the better) and calculate the expected rate of return.

If we expect earnings per share to grow at 12% in the next 10 years and the stock to trade at 40 times, the stock at its current price would give an annual return of 11.42%. If growth rate is 15%, the rate of return is going to be 14.40%. That's a profound story, isn't it?

So what if earnings grow at 10% and the stock trades at a multiple of 25? Do we like to earn 4.40% in the next decade? At 11% growth rate, which is the last 5-year average, with a multiple of 40, the rate of return is going to be 10.42%; at 8.50%, which is the last 10-year average, the rate of return is 7.93%. Such is life.