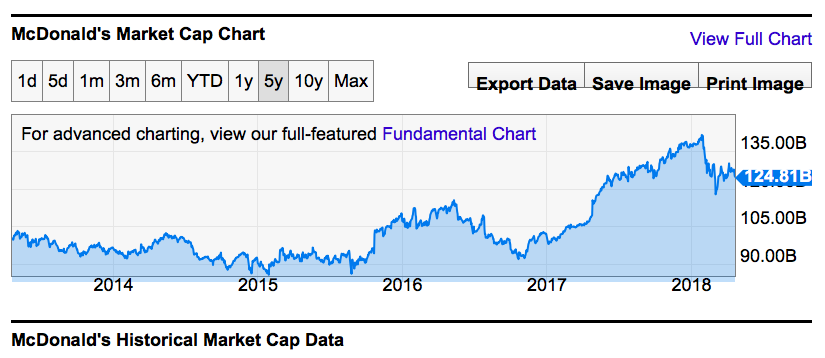

McDonald's Corporation is worth $125 b.

At its high stock prices in 2007, it was valued $74 b by the market; and at low prices, $49 b. That means, if you had bought the stock at high prices, the annualized rate of return isn't much to date. Even at low prices, the return is not tempting. But then again, who is good at market timing? If you check the past five years, the story is similar.

This is what happens with an aging business. Consider this: McDonald's revenues in 2007 were $22 b; they were $27 b in 2012; and revenues were $22 b in 2017. There is no growth in revenues for this burgers-and-fries business.

Reported operating profits were $3.8 b, $8.6 b, and $9.5 b in 2007, 2012, and 2017 respectively. When we adjust for leases and advertising costs, they change to $5 b, $9.5 b, and $10.1 b for the respective years. Adjusted operating margins look much better now (44%) compared to what they were in 2012 (34%), and in 2007 (22%).

Return on equity also improved significantly. For 2017, return on equity becomes meaningless as the equity turned negative in 2016. This is not alarming because it was due to excessive stock buybacks rather than accumulated losses. McDonald's is profitable and has healthy free cash flows.

Earnings per share were $2.06, $5.45, and $6.54 prior to adjustments for leases and advertising costs. When you capitalize leases and advertising costs, the EPS changes to $2.83, $6.16, and $6.97 for 2007, 2012, and 2017 respectively. While the 10-year annualized increase was in double digits rate, the 5-year increase has been very low. This is despite McDonald's huge stock buybacks over the years.

It repurchased 237 m shares in the past five years, and 465 m shares in the last 10 years. At the beginning of 2007, it had 1,203 m shares outstanding, which by the end of 2017 were 794 m. It is clear that if stock buybacks weren't carried out, earnings per share would have been lower, and of course, McDonald's would have retained its cash balance.

The future, though, doesn't look very bright for the business. Stephen Easterbrook surely has a task at hand. Where will he have to look?

Even the high growth markets aren't growing.

Free cash flows to firm were $2.6 b, $4.9 b, and $5.1 b for 2007, 2012, and 2017 respectively. Even if we consider $5 b as sustainable free cash flows to firm, we have debt to back out to arrive at equity values.

McDonald's had $29 b of long term book debt as of 2017. It also has long term leases which make up almost another $10 b of debt in present value terms. That is $39 b of total debt. With cash and other operating assets of $3.5 b, the net debt value is about $36 b.

To justify market value of $125 b for its equity, McDonald's operating assets will have to be worth about $165 b. With $5 b of FCFF, that implies a multiple of 33 times. And McDonald's isn't a growing business.

But then Tesla has never had free cash flows; it has never had operating profits; and had debt of $13 b as of 2017; yet, it's equity is worth $50 b. While McDonald's is aging, Tesla has survival issues to deal with.

Who are we to argue with the markets? We might as well profit out of their follies.

Who are we to argue with the markets? We might as well profit out of their follies.

No comments:

Post a Comment