I have written about valuation earlier. It is no secret that value of an asset is the present value of its future cash flows discounted at an appropriate rate. In other words, it is today's value of cash that can be taken out.

If there are no cash flows, there can be no value, period. There goes the so-called-valuation of precious items such as gold, silver, or even collection items, for a toss. You cannot value them, you can only price them.

Let's move to cash flow generating assets, in particular, stock of a business. The business will have cash flows until it is liquidated. A good business might have positive cash flows, and a bad one might have a stretch of negative cash flows. Yet, cash flows are what matter when we want to value the business.

Heck, both cash flows and discount rate to be used are difficult to estimate. For this reason, most of the analysts and investors use multiples to come up with pricing, and call it valuation. The expectations game and the timing game are routinely played in the market.

When we have constraints on estimating cash flows and discount rate, it makes sense to look for alternative approaches to investing. I noted how private equity investors expect return on their investment.

The more we think about valuation, the more we should accept the fact that no valuation is going to be perfect: The cash flows are going to be wrong; the discount rate is going to be wrong; and even more, the entire process is going to be colored by emotions; our greed, fear and envy at the point of valuation impact our estimates. It is hardly surprising that our valuation is not going to be right.

So what do we do? We still need an approach to make money off the markets, and if we believe that often markets are inefficient, there is all the more reason to think about ways to deal with that. Of course, for an investor with no time and interest, buying index is the best approach, that boring, low risk investing.

For the investor who has both time and interest in equity analysis, it is exciting, yet, the constraints remain the same: estimating cash flows and discount rate. Assuming that he can play the waiting game to deal with estimating cash flows, he still has to find a way to come up with the discount rate.

Here, the private equity approach comes handy. The academia and most of the analysts restricted by the institutional imperative use the CAPM to calculate the discount rate. The value investing camp rubbishes it, but fails to lay down an approach that can be used consistently. They like to take a dig at the rest of the world, but often, do something similar implicitly. For instance, they also use different discount rates for different cash flows streams, just like the CAPM guys; the CAPM guys are more explicit in their calculation of the discount rate, while the other camp is more implicit. There are other silly things that value investors do, which I will deal with another day.

I have no right answer to deal with the discount rate. Nevertheless, it is important to note that value of a business changes when we change the discount rate, sometimes significantly. Therefore, it is wise to be realistic when an investor uses the discount rate.

If the discount rate represents our opportunity cost for postponing present consumption, retaining (or increasing) purchasing power, or even dealing with the uncertainty in the future, we need an appropriate return on our investment. Going back to basics, an investor should expect a rate higher than the government treasury, a rate higher than high quality debt instrument, and also a rate higher than the market rate.

If this is acceptable, we can come up with a way to accept the discount rate too. Here's how.

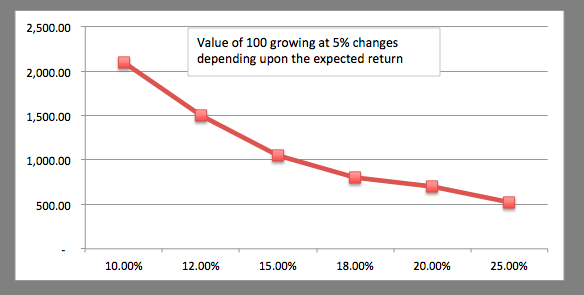

The value of a business with cash flows of 100 growing at 5% perpetually changes as we change our expected return. If its stock is trading at 1,500, at 10% expected return value is higher than price. The question to ask, however, is whether 10% return is acceptable. We could buy government treasury or a high quality bond for that return. If we buy at the current price, the expected return is 12%, is that adequate considering our opportunity costs? If the expected return is 15%, the price has to come down by 30% to 1,050; but wait, can't we get that return by just buying the index? I reckon, for a selective stock picking investor, the expected return cannot be lower than market returns. Therefore, he will have to ask for more than that. Let's start with 18%; for this return, the market price has to come down by 46% to 807.

In fact, this simple model can be extended to the standard DCF model, using cash flows and growth rate that are demonstrable for the business until it becomes mature, and after that using return on capital, growth rate, reinvestment, and cash flows that characterize the stable business.

Here, the private equity approach comes handy. The academia and most of the analysts restricted by the institutional imperative use the CAPM to calculate the discount rate. The value investing camp rubbishes it, but fails to lay down an approach that can be used consistently. They like to take a dig at the rest of the world, but often, do something similar implicitly. For instance, they also use different discount rates for different cash flows streams, just like the CAPM guys; the CAPM guys are more explicit in their calculation of the discount rate, while the other camp is more implicit. There are other silly things that value investors do, which I will deal with another day.

I have no right answer to deal with the discount rate. Nevertheless, it is important to note that value of a business changes when we change the discount rate, sometimes significantly. Therefore, it is wise to be realistic when an investor uses the discount rate.

If the discount rate represents our opportunity cost for postponing present consumption, retaining (or increasing) purchasing power, or even dealing with the uncertainty in the future, we need an appropriate return on our investment. Going back to basics, an investor should expect a rate higher than the government treasury, a rate higher than high quality debt instrument, and also a rate higher than the market rate.

If this is acceptable, we can come up with a way to accept the discount rate too. Here's how.

The value of a business with cash flows of 100 growing at 5% perpetually changes as we change our expected return. If its stock is trading at 1,500, at 10% expected return value is higher than price. The question to ask, however, is whether 10% return is acceptable. We could buy government treasury or a high quality bond for that return. If we buy at the current price, the expected return is 12%, is that adequate considering our opportunity costs? If the expected return is 15%, the price has to come down by 30% to 1,050; but wait, can't we get that return by just buying the index? I reckon, for a selective stock picking investor, the expected return cannot be lower than market returns. Therefore, he will have to ask for more than that. Let's start with 18%; for this return, the market price has to come down by 46% to 807.

Logically then, the investor would wait for the price to come to 807 or lower to provide adequate return to his investment. For any lower returns, he has alternative investments available. So that means the investor will have to happily come back to my favorite, the waiting game.

The concluding thoughts: The investor cannot come up with an accurate value of the business given the constraints on the precise discount rate. Rather than attempting to value, he should wait for the prices to reach to his level of expectations. The investor should not calculate the discount rate using the CAPM like the academia and institutional analysts, and he should rather not use an arbitrary discount rate like the value investing camp.

What he should do is wait for the price to fall - and there will be occasions considering efficiencies in the market - before he can buy any stock so that he will get adequate return on his investment.

What is the point in swinging routinely, just for the heck of it? Don't we have better things to do in life?

The concluding thoughts: The investor cannot come up with an accurate value of the business given the constraints on the precise discount rate. Rather than attempting to value, he should wait for the prices to reach to his level of expectations. The investor should not calculate the discount rate using the CAPM like the academia and institutional analysts, and he should rather not use an arbitrary discount rate like the value investing camp.

What he should do is wait for the price to fall - and there will be occasions considering efficiencies in the market - before he can buy any stock so that he will get adequate return on his investment.

What is the point in swinging routinely, just for the heck of it? Don't we have better things to do in life?

No comments:

Post a Comment