The business

The company had revenues of Rs.94 b, operating earnings of Rs.8 b and net earnings of 9.7 b for the year ended 31 March 2016. There were operating losses during the previous year. The company says it is the second largest spirit company in the world and the largest one in India. 93 m cases were produced during the financial year that ended. It has a portfolio of over 140 brands, with 15 brands having sales of over 1 m cases and 3 brands with over 10 m cases. Pretty solid.

The company had revenues of Rs.94 b, operating earnings of Rs.8 b and net earnings of 9.7 b for the year ended 31 March 2016. There were operating losses during the previous year. The company says it is the second largest spirit company in the world and the largest one in India. 93 m cases were produced during the financial year that ended. It has a portfolio of over 140 brands, with 15 brands having sales of over 1 m cases and 3 brands with over 10 m cases. Pretty solid.

United Spirits is in the business of manufacture, sale and distribution of alcohol beverages, predominantly in India. It has 19 subsidiaries, one associate and 74 manufacturing facilities. The business strategy is in the process of a significant change since Diageo took full control of the business in July 2014. Diageo is a global leader in alcohol beverages with a collection of premium brands and operates across the world.

United Spirits:

Diageo:

United Spirits:

Diageo:

The market

Alcohol beverages market includes beer, distilled spirits and wine. In India it also includes country liquor. United Spirits is primarily into India made foreign liquor (IMFL) market, which accounts for 70% of the total market, and the company has a market share of 40% in volumes and 50% in value.

Alcohol beverages market includes beer, distilled spirits and wine. In India it also includes country liquor. United Spirits is primarily into India made foreign liquor (IMFL) market, which accounts for 70% of the total market, and the company has a market share of 40% in volumes and 50% in value.

Whisky leads both the total market and the IMFL market in India. Beer is the second widely consumed alcohol beverage.

While both popular and premium brands have a ready market, premium brands are gaining market share, albeit slowly. Premium brands also enjoy better margins; therefore, contribute higher to the operating earnings.

United Spirits competes with Pernod Ricard in premium segment and with Radico Khaitan and Tilaknagar Industries in popular segment. Allied Blenders and Distillers is also a competitor. United Spirits lags its competitors in terms of operating margins. Surely, something must have gone wrong for the company.

The decade that went past

The company has not performed well in the past due to several reasons: increasing burden of excise duties, high debt, inefficient working capital management, increasing raw material prices and bad business execution. It also has had corporate governance issues.

The decade that went past

Revenues increased 5% annually in the past 5 years and about 16% in the past 10 years. In 2014, the company impaired Rs.32 b goodwill recognized during its acquisition of Whyte and Mackay. This is what happens when you buy for GBP 600 m in 2007 and sell for GBP 430 m in 2014. High finance costs have been a drag on the company's performance.

Both operating and net margins have been falling.

All this has had an obvious impact on the earnings per share.

Market price

The story so far has been clear: bad. Yet, the market value of equity has not quite reflected it. So far in 2016, it was valued as high as Rs.585 b and as low as Rs.324 b. Even the lower price has an implied PE of over 33.

The story so far has been clear: bad. Yet, the market value of equity has not quite reflected it. So far in 2016, it was valued as high as Rs.585 b and as low as Rs.324 b. Even the lower price has an implied PE of over 33.

As of now, the company is valued by the market at Rs.335 b implying high multiples of its current earnings. Why so? Probably because markets look into the future and discount all information that is available. Efficient market hypothesis, I guess. Here, the market is probably thinking that Diageo will fix all the problems and make the business profitable.

Enter Diageo

The good news, however, is that since Diageo took over control, there have been things that are positive for the business. Now the operating margin is at 8.52% and net profits margin is at 10.32%. EPS is Rs.66.59. Return on capital is 12.96% and return on equity is 146% mainly due to the clean-up of bad assets. Diageo has sold Whyte and Mackay which accounted for 16% of revenues and shares held in United Breweries. Debt is lower than before. It has also brought in changes to the management and the board.

With the current numbers if we try to value the business, the market price appears too high. That means we need to assume much better picture going forward. The operating and net margins will have to go up, revenues will have to grow at a much higher rate. Reinvestment has to be based on efficient use of capital.

Highly regulated; no pricing power

Can this happen for a business which is highly regulated, and laden with high debt and working capital requirements?

Consider this: The company is operating in an environment where the government is involved in licensing, production (setting up the plant), distribution (wholesale and retail) and pricing of products. There are taxes even for the inter-state movement of liquor.

In addition, at least four states have already banned liquor, and Kerala and Tamil Nadu are in the process of implementing the ban. Tamil Nadu has already become a troubled market for United Spirits with limits on volume sales in the state.

The government has also tried to affect the prices of ethanol (which is about 40% of raw materials cost) adversely for United Spirits.

Direct advertisement is not possible for the liquor business. So only people with liquor-sense would appreciate those indirect advertisements which cost about 10% of revenues annually.

Excise duty as a percentage of revenues has increased from 43% in 2006 to 59% in 2016. The company paid Rs.134 b in excise duties for the year 2016 and a total of Rs.801 b in the last 10 years.

Excise duty is a major revenue for the state governments. The fact that liquor has been excluded from GST in its current form says something.

Finally, lack of adequate pricing power puts any business in jeopardy.

Where are the competitive advantages?

The biggest negative is also the biggest positive for United Spirits. Because the industry is highly regulated, there is a huge entry barrier. It is very difficult for a new player to obtain licenses, set up plants and distribution channels across the country and price the products to achieve positive net present value of its cash flows.

Then there are other positives as noted by management and analysts: Demographic structure, low per-capita consumption compared to the world average, rising disposable income, portfolio of brands, production and distribution facilities and Diageo at the top to steer the wheel.

Focus on premium brands

Diageo has plans to repackage the company's top brands and introduce to the market in a more prominent manner. It expects to increase market share of premium brands which are currently 37% (volume) and 51% (value).

It has already sold non-core assets to reduce debt which is Rs.42 b as of now. Management has projected that revenues have the potential to increase by 13% in the next five years. Diageo has an operating margin of 28% compared to United Spirit's 8.52%. I am not sure what will be the sustainable target operating margin. I don't think there is much scope for improvement in reinvestment though; current capital generates revenues 1.65 times. While there is scope for working capital efficiencies, overall capital requirements should be in line with the industry average.

Value and price

I tried to value United Spirits with discounted cash flows and found that market price was quite high. It might be interesting to try to price the stock. In 5 out of last 10 years, the company had negative EPS. I don't want to give too much emphasis on the past. Let's say that its current EPS of Rs.66.59 grows at 12% in the next 10 years. Market price in year 10 then would be a function of the PE multiple applied for the stock.

And the buy price of the stock would be a function of expected rate of return:

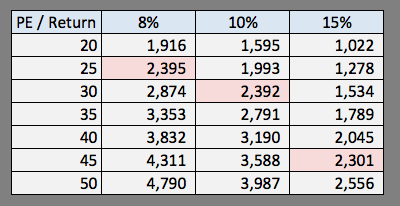

Based on the current market price, for instance, if the investor's expected rate of return is 8%, the stock would have to be priced at a PE multiple of 25 at year 10; any higher multiple will increase the rate of return. Is 8% good enough? We don't know especially with the lower inflation and interest rates environment anticipated. For each investor his or her own opportunity cost. I have not factored dividends, if any, in the cash flows; that will be an additional return.

If the expected rate is 10%, the stock would have to be priced at 30 times earnings; and for 15% return, it should be 45 times. The stock has been priced at higher than this multiple many times in the past. In 2016 itself it was priced at about 60 times earnings. If the stock is really going to give an EPS growth of 12% over next 10 years, it would be a high performing stock warranting a higher multiple. How much higher is anybody's guess.

Now these expected prices are based on the performance of 12% growth in EPS. It will be phenomenal if it actually happens, but we are not sure. It could as well be lower. My guess is as good as anybody's. We can price the stock with the lower growth rate too.

The Diageo ride

There is some comfort that one can take if it sounds acceptable. Diageo acquired controlling stake in the business in 2013 and 2014. First it acquired 36 m shares in United Spirits based on a preferential allotment at Rs.1440 per share in 2013. Next it acquired 1.96 m shares at Rs.2400 per share and after that 3.5 m shares at Rs.2474.45 per share from the market. Finally it acquired 37.78 m shares at Rs.3030 per share through a tender offer in July 2014. Its average cost of acquisition of 79.61 m shares (54.78% control) was Rs.2263.86 per share.

This price is close to the current market price. An investor who buys United Spirits stock today will ride along with Diageo in the future. Diageo has noted that it expects its acquisition to be economic profits positive in year 5 assuming 12% cost of capital. Is it that its investment should give a return of 12% in the next 5 years? Whatever that means. I have also written about United Spirits earlier.

The challenges

With entry barriers as the primary long term competitive advantage and brands as the secondary, Diageo will have a test of time.

There is a plethora of qualifications and emphasis of matters from the auditors highlighting breaches of historical agreements, and deficiencies in control environment and corporate governance. New management will have to tackle all this to enhance the image of the company and its business. United Spirits has contingent liabilities of Rs.11.8 b as of 2016. A portion of this might as well be cash outflows in the coming years.

Goodwill

The balance sheet includes Rs.1.12 of goodwill; it is not clear which acquisition it pertains to. Since Diageo has impaired significant value of goodwill where the present value of cash flows were much lower, we can assume that the current carrying value of goodwill is value accretive.

IPL franchise

The carrying value of IPL franchise rights was Rs.3.9 b, and these are surprisingly grouped under operations. Whenever the game of cricket became part of the liquor business operations we cannot tell. The revenues of Rs.1.35 b and direct costs of Rs.1.08 b are classified under operating revenues and operating expenses respectively. There are additional costs related to the franchise probably resulting in a loss for the year. Ideally, these should be separated and shown under other income. We cannot include IPL revenues in cash flows and project it as part of liquor beverage business. Nevertheless, the market value of franchise rights is probably higher than its carrying value.

Diageo India

Diageo also operates independently in India as a private business. There is no clarity as to why this has not merged with United Spirits and how it is going to affect United Spirits operations.

The 12% growth

The job for Anand Kripalu and Diageo is cut out: 1) Increase revenues; 2) Increase operating margin; 3) Reduce debt; 4) Efficiently reinvest capital; 5) Do not dilute equity. These efforts should lead to increase in earnings per share.

The good news, however, is that since Diageo took over control, there have been things that are positive for the business. Now the operating margin is at 8.52% and net profits margin is at 10.32%. EPS is Rs.66.59. Return on capital is 12.96% and return on equity is 146% mainly due to the clean-up of bad assets. Diageo has sold Whyte and Mackay which accounted for 16% of revenues and shares held in United Breweries. Debt is lower than before. It has also brought in changes to the management and the board.

With the current numbers if we try to value the business, the market price appears too high. That means we need to assume much better picture going forward. The operating and net margins will have to go up, revenues will have to grow at a much higher rate. Reinvestment has to be based on efficient use of capital.

Highly regulated; no pricing power

Can this happen for a business which is highly regulated, and laden with high debt and working capital requirements?

Consider this: The company is operating in an environment where the government is involved in licensing, production (setting up the plant), distribution (wholesale and retail) and pricing of products. There are taxes even for the inter-state movement of liquor.

In addition, at least four states have already banned liquor, and Kerala and Tamil Nadu are in the process of implementing the ban. Tamil Nadu has already become a troubled market for United Spirits with limits on volume sales in the state.

The government has also tried to affect the prices of ethanol (which is about 40% of raw materials cost) adversely for United Spirits.

Direct advertisement is not possible for the liquor business. So only people with liquor-sense would appreciate those indirect advertisements which cost about 10% of revenues annually.

Excise duty as a percentage of revenues has increased from 43% in 2006 to 59% in 2016. The company paid Rs.134 b in excise duties for the year 2016 and a total of Rs.801 b in the last 10 years.

Excise duty is a major revenue for the state governments. The fact that liquor has been excluded from GST in its current form says something.

Finally, lack of adequate pricing power puts any business in jeopardy.

Where are the competitive advantages?

The biggest negative is also the biggest positive for United Spirits. Because the industry is highly regulated, there is a huge entry barrier. It is very difficult for a new player to obtain licenses, set up plants and distribution channels across the country and price the products to achieve positive net present value of its cash flows.

Then there are other positives as noted by management and analysts: Demographic structure, low per-capita consumption compared to the world average, rising disposable income, portfolio of brands, production and distribution facilities and Diageo at the top to steer the wheel.

Focus on premium brands

Diageo has plans to repackage the company's top brands and introduce to the market in a more prominent manner. It expects to increase market share of premium brands which are currently 37% (volume) and 51% (value).

It has already sold non-core assets to reduce debt which is Rs.42 b as of now. Management has projected that revenues have the potential to increase by 13% in the next five years. Diageo has an operating margin of 28% compared to United Spirit's 8.52%. I am not sure what will be the sustainable target operating margin. I don't think there is much scope for improvement in reinvestment though; current capital generates revenues 1.65 times. While there is scope for working capital efficiencies, overall capital requirements should be in line with the industry average.

Value and price

I tried to value United Spirits with discounted cash flows and found that market price was quite high. It might be interesting to try to price the stock. In 5 out of last 10 years, the company had negative EPS. I don't want to give too much emphasis on the past. Let's say that its current EPS of Rs.66.59 grows at 12% in the next 10 years. Market price in year 10 then would be a function of the PE multiple applied for the stock.

And the buy price of the stock would be a function of expected rate of return:

Based on the current market price, for instance, if the investor's expected rate of return is 8%, the stock would have to be priced at a PE multiple of 25 at year 10; any higher multiple will increase the rate of return. Is 8% good enough? We don't know especially with the lower inflation and interest rates environment anticipated. For each investor his or her own opportunity cost. I have not factored dividends, if any, in the cash flows; that will be an additional return.

If the expected rate is 10%, the stock would have to be priced at 30 times earnings; and for 15% return, it should be 45 times. The stock has been priced at higher than this multiple many times in the past. In 2016 itself it was priced at about 60 times earnings. If the stock is really going to give an EPS growth of 12% over next 10 years, it would be a high performing stock warranting a higher multiple. How much higher is anybody's guess.

Now these expected prices are based on the performance of 12% growth in EPS. It will be phenomenal if it actually happens, but we are not sure. It could as well be lower. My guess is as good as anybody's. We can price the stock with the lower growth rate too.

The Diageo ride

There is some comfort that one can take if it sounds acceptable. Diageo acquired controlling stake in the business in 2013 and 2014. First it acquired 36 m shares in United Spirits based on a preferential allotment at Rs.1440 per share in 2013. Next it acquired 1.96 m shares at Rs.2400 per share and after that 3.5 m shares at Rs.2474.45 per share from the market. Finally it acquired 37.78 m shares at Rs.3030 per share through a tender offer in July 2014. Its average cost of acquisition of 79.61 m shares (54.78% control) was Rs.2263.86 per share.

This price is close to the current market price. An investor who buys United Spirits stock today will ride along with Diageo in the future. Diageo has noted that it expects its acquisition to be economic profits positive in year 5 assuming 12% cost of capital. Is it that its investment should give a return of 12% in the next 5 years? Whatever that means. I have also written about United Spirits earlier.

The challenges

With entry barriers as the primary long term competitive advantage and brands as the secondary, Diageo will have a test of time.

There is a plethora of qualifications and emphasis of matters from the auditors highlighting breaches of historical agreements, and deficiencies in control environment and corporate governance. New management will have to tackle all this to enhance the image of the company and its business. United Spirits has contingent liabilities of Rs.11.8 b as of 2016. A portion of this might as well be cash outflows in the coming years.

Goodwill

The balance sheet includes Rs.1.12 of goodwill; it is not clear which acquisition it pertains to. Since Diageo has impaired significant value of goodwill where the present value of cash flows were much lower, we can assume that the current carrying value of goodwill is value accretive.

IPL franchise

The carrying value of IPL franchise rights was Rs.3.9 b, and these are surprisingly grouped under operations. Whenever the game of cricket became part of the liquor business operations we cannot tell. The revenues of Rs.1.35 b and direct costs of Rs.1.08 b are classified under operating revenues and operating expenses respectively. There are additional costs related to the franchise probably resulting in a loss for the year. Ideally, these should be separated and shown under other income. We cannot include IPL revenues in cash flows and project it as part of liquor beverage business. Nevertheless, the market value of franchise rights is probably higher than its carrying value.

Diageo India

Diageo also operates independently in India as a private business. There is no clarity as to why this has not merged with United Spirits and how it is going to affect United Spirits operations.

The 12% growth

The job for Anand Kripalu and Diageo is cut out: 1) Increase revenues; 2) Increase operating margin; 3) Reduce debt; 4) Efficiently reinvest capital; 5) Do not dilute equity. These efforts should lead to increase in earnings per share.

No comments:

Post a Comment